![]()

![]()

Welcome to this newsletter from the Customer Union for Ethical Banking, the independent union for customers of The Co-operative Bank and Coventry Building Society.

In this month’s newsletter: a flavour of our survey results; Coventry makes a packet on the Co-op; and the bank’s own survey gets us a bit worked up… Plus, is Smile on the way out?

Our survey showed…

Thanks to all of you who filled out our survey – we had over 800 responses, close to 10% of our newsletter subscribers. We really appreciate this high level of engagement from you.

To give you a flavour of the responses, it’s clear that there is strong support for the Co-op/Coventry merger, with 72% support (agree or strongly agree) and only 1% opposed. However the significant number (22%) who neither agree nor disagree does indicate some uncertainty about what the merger means in practice.

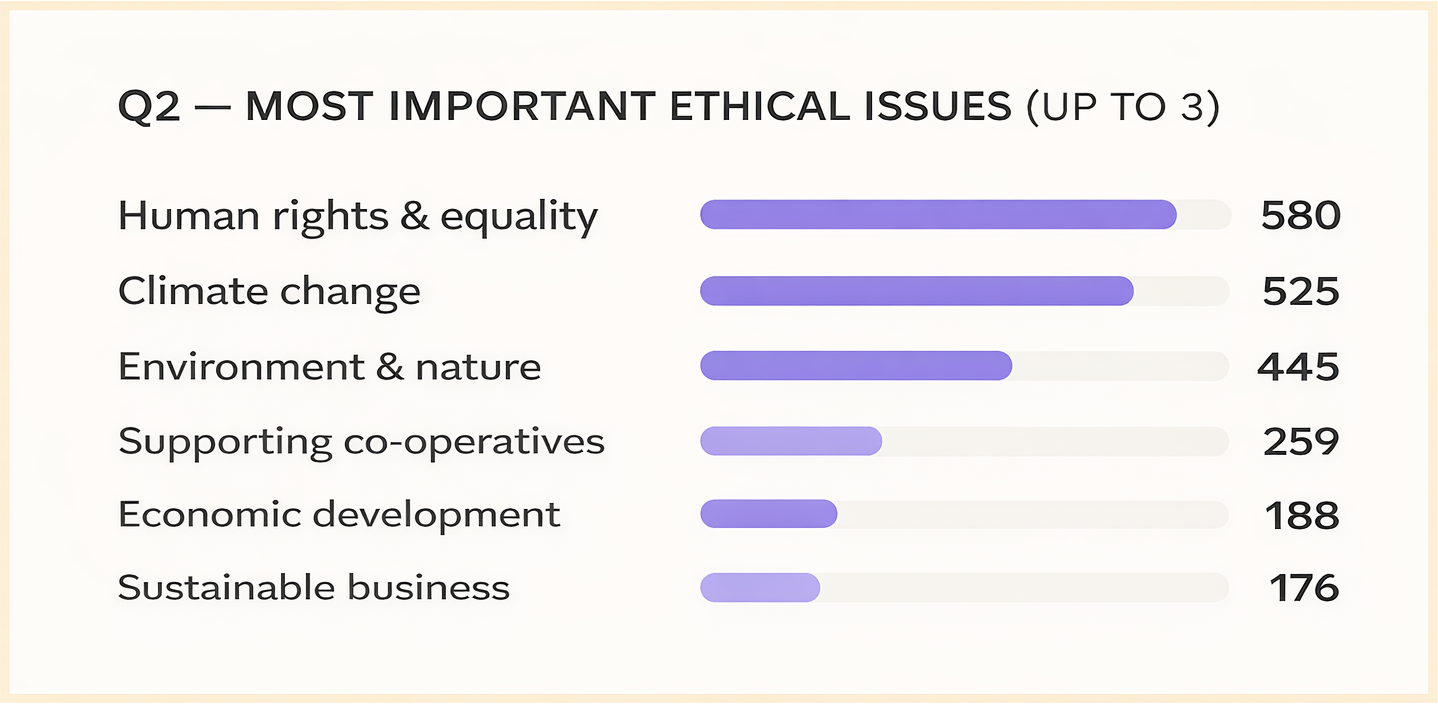

And 89% of respondents agree or strongly agree that the bank is a clear leader in ethical banking. However, more “agree” than “strongly agree”, reflecting that the bank perhaps still has some work to do to make sure we are convinced! Also, 66% said that joining the Customer Union made you more likely to stay with the bank over the years. We were also interested and encouraged to see that you put human rights and equality at the top of the list of most important issues, slightly above climate change – reinforcing the idea that the Co-op needs to focus on both these areas.

One important reason we wanted to conduct this survey is to hear from members and supporters that might not join our annual gatherings. Since some 90% of our respondents had never attended a gathering, the results give us some useful food for thought about how we might expand involvement and hear from more of you in other ways.

Coventry profits grow on merger

As the FT Adviser reports, Coventry Building Society saw a significant rise in profits for 2025, the first full year following its acquisition of the Co-op Bank. Coventry’s own news release says its “statutory profit before tax increased to £801 million (2024: £323 million), including a gain of £584 million on the acquisition of The Co-operative Bank (‘the Bank’). The day one gain reflects the agreed purchase consideration being over 40% below the fair value of the net assets acquired.”

This looks like Coventry paid £780 million for a bank worth more like £1.3 billion, which would imply they got a good deal! Members of our expert panel tell us this is not so unusual, as the hedge funds selling the Co-op Bank had no way to capture the benefits of combining two complementary businesses. Coventry on the other hand, can unlock additional value from buying the bank because of these synergies. While accounting rules require this anticipated gain to be recognised upfront, whether it fully materialises will only become clear over the coming years.

Co-op’s own survey lumps charities and coops

Some of us have had an email from the bank recently inviting us to “Have your say in the Charity Banking Survey 2026.” This was frustrating for those of us who are involved with co-operatives and not with charities!

We contacted the bank about this and heard that it went to all customers with a Charity and Community Account, so it was also intended for co-operatives.

The Co-operative Bank should know better than to lump co-operatives and charities together. Coops are not charities, and the bank should know this. It should be speaking to cooperatives properly, and show it understands the sector.

We would like it to run the survey opportunity again, specifically requesting input from co-ops this time.

We asked the bank if they wanted to comment and they told us:

"We recently shared an opportunity for a cohort of customers to contribute to Charity Finance’s annual survey, which invites organisations to share their views on their banking experience with any UK bank. This survey is created and owned entirely by Charity Finance. Our email to customers simply highlighted the opportunity to take part; it was not a Co-operative Bank survey.

"We recently shared an opportunity for a cohort of customers to contribute to Charity Finance’s annual survey, which invites organisations to share their views on their banking experience with any UK bank. This survey is created and owned entirely by Charity Finance. Our email to customers simply highlighted the opportunity to take part; it was not a Co-operative Bank survey.

Due to the similarity of names across co-operative and charity organisations, it is not always possible for us to distinguish between the two groups within our marketing data. As a result, some co-operatives may have received the invitation. Our intention was to ensure that any customer who wished to participate had the chance to do so.

This campaign does not reflect a lack of understanding of, or commitment to, the co-operative sector. Over the last decade, we have invested more than £3.5 million in supporting and developing co-operatives through the Business Support for Co-ops programme. We value our relationships with co-operatives and are committed to engaging with the sector in ways that reflect its unique strengths and needs.”

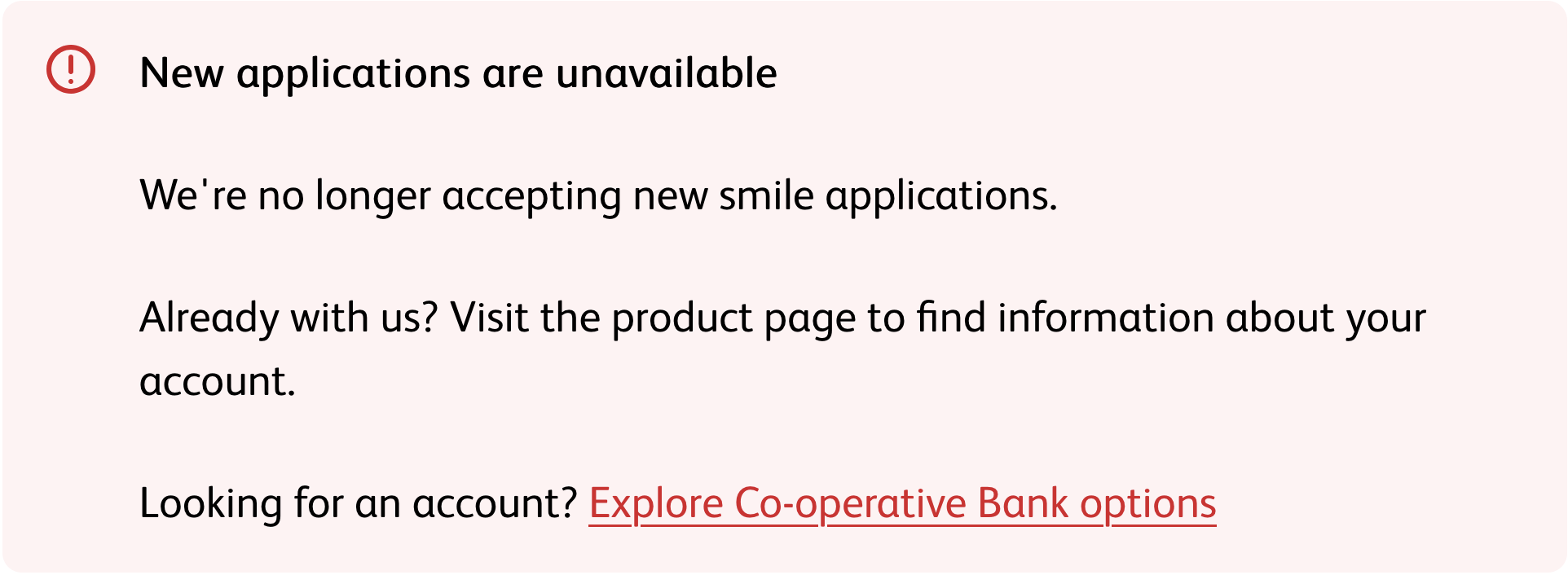

Smile new applications unavailable

Finally, we noticed that Smile, the Co-op’s online-only banking brand, is no longer taking new applications. Our members are asking, is the bank retiring the brand?

In a world of online-only “challenger banks” gaining market share, Smile – the UK’s first digital-only bank – reminds us that there was a time when the Co-op was a tech innovator! Perhaps they can be again?

We asked the bank for a reaction and they said:

"While existing smile customers can continue using their accounts as usual, we’ve decided to stop offering the smile current account, no-notice savings and cash ISA to new customers for the time being. For new customers, we have a broad range of products and services to offer through The Co-operative Bank to suit their needs - available online, via our app, by phone or in branch.”

With best wishes

The Customer Union team

Have you joined the Customer Union yet? It costs £15 a year to be a member of the first ever customer union co-operative, and help us ensure the Co-op Bank sticks to its principles. We also welcome Coventry Building Society members. It only takes a few moments to sign up here.

This version of the newsletter was modified following clarification from the bank on the integration process and timing.

@cuebcustomerunion.bsky.social

@cuebcustomerunion.bsky.social @saveourbank

@saveourbank